EVERYONE should file a FAFSA but not everyone should file the CSS Profile. One of the biggest mistakes is assuming you make too much money to file the Free Application for Federal Student Aid (FAFSA).

Whether your child is getting ready for the first year of college or the last year at high school, this is an important time for you. While your child focuses on studying, you have to worry about paying the college bills.

And applying for aid isn’t easy. In addition to keeping an eye on your child’s grades and exam results, your family will also need to review all of your tax and financial assets to ensure that you can afford the fees that the college demands.

Here are the five most important facts about financial aid:

1. October 1st is not the deadline….it’s the start time.

While it’s certainly best to get your FAFSA and Financial Aid Profiles in as early as possible (the first few weeks of October), not everyone manages to complete all their paperwork on time. The FAFSA October 1st is the start date and not the deadline. It is in your best interest to file as early as possible but not mandatory.

If Spring of Senior year is rolling around, it is still possible for you to get the help you need. The official deadline for FAFSA is June 30th. But don’t delay too long! You do need to get those forms in quickly. It’s very likely that a large chunk of the available funds will already be disbursed. The most important thing to understand is that many colleges won’t consider funding applications from parents who didn’t apply for aid during their child’s freshman year.

If you don’t send off your forms now, you could well find yourself cut out of college funding help for your child’s entire college career.

2. Forms Must Be Filed EVERY Year for EVERY Child

Many parents believe that once they’ve completed their financial aid forms and received their answers, their work is done. However, your financial situation can change from year to year. You could get a pay raise or a promotion that increases your income. The financial aid administration is fully aware of this. They’ll want to see your financial situation before the start of every school year. It’s important to remember that the financial aid process doesn’t stop at the beginning of the freshman year, it continues every year your child is in college.

3. There are No ‘Income Limits’ for Financial Aid

YOU DO NOT MAKE TOO MUCH MONEY TO POTENTIALLY GET AID. Financial aid comes in two forms: need-based aid and merit-based aid. Obviously, high-earning families are unlikely to receive much, if any, need-based aid. But they can certainly get a share of the other funds. When the financial aid administration allocates loans and scholarships etc., they don’t only look at income. For example, they may take into account the extra expenses of having multiple children in college. They may even look at your age to see if you qualify for additional help.

It’s also possible to position your assets so that when your application is submitted you present your best financial front. In fact, if you take the correct action now, you might find that it’s possible to fund your child’s education, pay off your mortgage, keep saving for your retirement, and maintain your current lifestyle.

The financial aid process can actually give some people an opportunity to do all of this. However, not every financial professional will know how to fully handle this situation. You will need an experienced professional or, more likely, a team, to assist with this type of financial allocation. Is your team helping you save ON the cost of college or have they just provided a plan to save FOR the cost of college. If it is the latter, you might need a second opinion.

4. Private Scholarships Are Rarely the Answer

When most people think of college aid, one of the first solutions that comes to mind are private scholarships. Scholarships are sometimes awarded for academic or athletic excellence. They can also be used to help disadvantaged sectors of society. All count as free money.

However, scholarships are very rare. About 97 percent of financial aid is made up of grants or loans from the state government, the federal government, or from universities. Only about 3% comes in the form of private scholarships. That’s unlikely to even cover your child’s yearbook expenses, let alone a complete college degree.

Of course, you shouldn’t ignore scholarships either. Every little bit helps and if you have some spare time, you might find some interesting opportunities with independent research. But remember, even if your child receives a scholarship, the school may reduce its own package by the amount of the award. Be sure to ask the school how they view outside scholarship. Will it be considered an additional family resource hurting your aid or will it be something you can use to further lower your costs.

Start your search: http://www.collegescholarships.org/financial-aid/

5. You Must Understand Financial Aid Vocabulary

Even financial experts can feel a little lost when it comes to applying for financial aid. There are all sorts of special terms that just don’t turn up anywhere else. In college planning, these terms will come up again and again. You must know what they mean:

Expected Family Contribution (EFC)

There are two kinds of Expected Family Contribution (EFC): The federal EFC is the amount the government thinks that you should pay, and the institutional EFC is the amount that private schools and colleges think you should pay. The higher your EFC, the bigger your college expenses. Your EFC is comprised primarily from parent income, parent assets, student income, and student assets.

Base Financial Year

Your Base Financial Year is based on some called the “prior-prior” year. To simplify, the formula uses your tax return two years prior to your student’s high school graduation year. Example: High school student graduates in 2018, you will use your 2016 income tax return to file the FAFSA in 2017. Crazy right? This is only the income piece. Your asset information will be based on the balance at the time you file, potentially providing an opportunity to improve your chances to increasing your aid.

A few examples might be moving college assets from the student’s name to the parent’s name. If you’ve got a big expense such as a roof repair or a new car purchase coming up, you could be better off paying the bill before you fill in the forms so that that money is no longer counted as savings. Please do not employ these strategies before consulting with a professional since this might be a big mistake depending on your family’s financial situation.

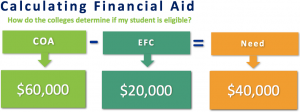

COA

COA= Cost of Attendance is comprised of room & board, tuition, books and other related college expenses. This number is for one year and most importantly is just a sticker price. Just because the school advertises at COA of $65,000 doesn’t mean that is what your family will pay.

Knowing your financial fit first will allow you to potentially look at schools with high sticker prices or identify ones that provide your student merit aid (free money regardless of your income).

Need

“Need” on financial aid forms is the difference between your EFC and the cost of sending your child to a particular school. The size of your need will depend on the college and your EFC amount. The higher your need, the more aid you may be eligible for. Whether your child is preparing for college or getting ready for his or her senior year of high school, you’re not alone at this difficult time.

Understanding this formula can help your student obtain their dream college.